In the world of healthcare policy, we often celebrate “wins” that look great on a campaign flyer or a news ticker. The $35 monthly cap on insulin is exactly that. It is a monumental step forward, and as someone who has spent years researching social justice and the legal frameworks of our healthcare system, I genuinely view it as a triumph for millions of families.

However, if my time at Brandeis and Columbia taught me anything, it is that a “cap” is often just a lid on a much deeper, more complex pot. While the $35 price point has provided immediate relief for many, it hasn’t necessarily fixed the structural cracks underneath. As we move through 2026, we are seeing that the “crisis” hasn’t disappeared, it has just changed shape.

In this post, I want to pull back the curtain on what the $35 cap doesn’t cover, why racial and socioeconomic disparities are still persisting despite the lower price, and what the next phase of insulin advocacy actually looks like.

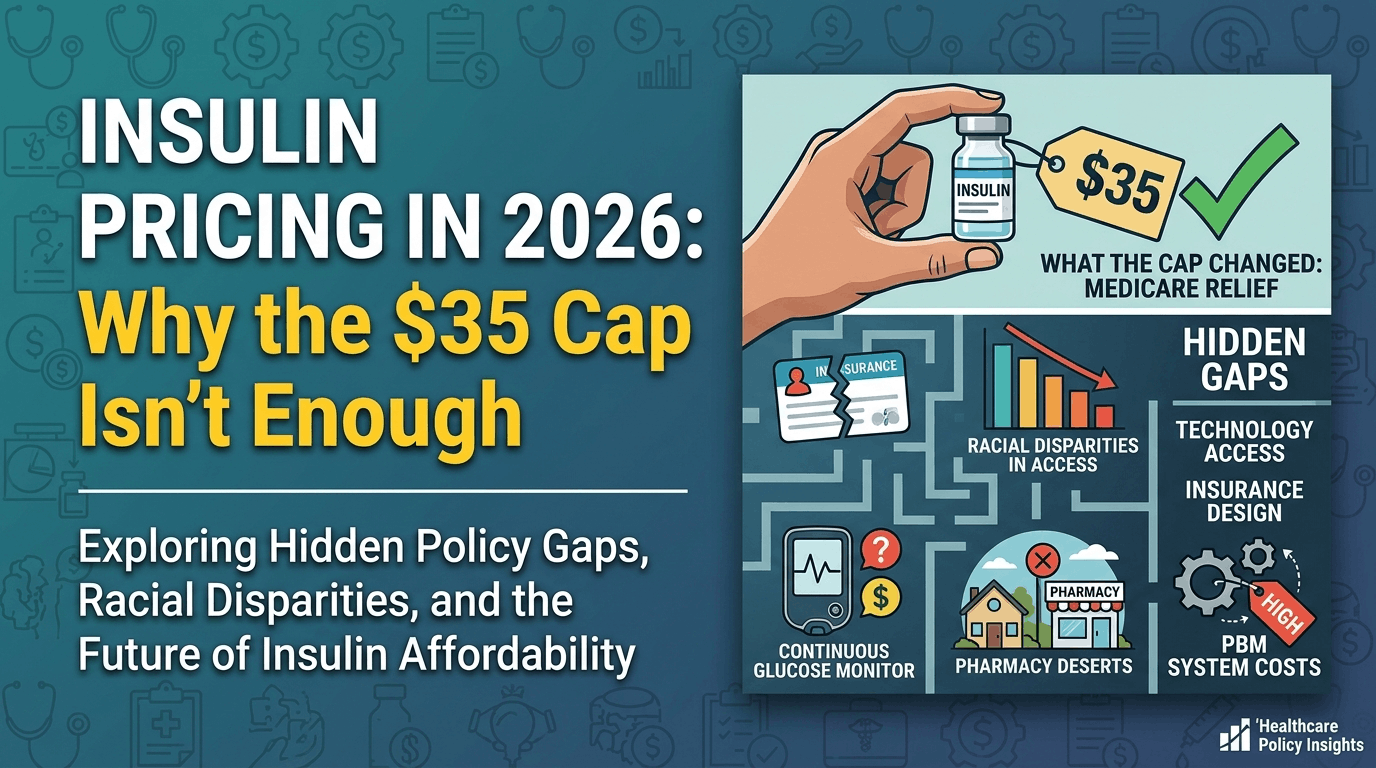

The 2026 Snapshot: What the Cap Actually Changed

The $35 cap significantly reduced out-of-pocket costs for many Medicare patients. Before the reform, insulin affordability varied widely depending on insurance coverage and rebate structures. Below is a simplified comparison of typical out-of-pocket costs before and after the policy.

| Period | Typical Monthly Out-of-Pocket Cost | Who Was Most Affected |

| Before the Cap | $58–$63 average; uninsured patients often paid $100+ per vial | Medicare patients and uninsured individuals |

| After the Cap | $35 per month per covered insulin product | Medicare beneficiaries under Part B and Part D |

The change was meaningful. Key outcomes of the policy include:

- Predictable monthly costs for Medicare patients

- Reduced financial stress for seniors with diabetes

- Stronger federal involvement in drug pricing negotiations

- Expanded national debate on pharmaceutical pricing transparency

However, one word in the policy continues to shape its limits: “Covered.” The cap applies only to certain insurance structures. Patients outside those frameworks still navigate a fragmented system.

The Coverage Gap: Patients Outside the System

Many insulin manufacturers, such as Eli Lilly, Novo Nordisk, and Sanofi, introduced voluntary programs mirroring the federal cap. These initiatives lowered costs for some commercially insured patients. But unlike federal mandates, manufacturer programs often depend on:

- Savings cards

- eligibility verification

- enrollment limits

- temporary discount structures

For people with stable employer insurance, this system can work. For others, it can feel uncertain. Patients who frequently encounter coverage instability include:

- Gig economy workers

- Individuals between jobs

- Freelancers without employer insurance

- Young adults aging out of parental coverage

For these groups, insulin affordability often depends on navigating manufacturer programs that can change or expire. Even in 2026, access to life-sustaining medication can still hinge on how well someone navigates insurance fine print.

Why Lower Prices Haven’t Closed Health Disparities

Reducing the price of insulin addresses one important barrier, but diabetes outcomes depend on much more than medication costs alone. Public health research continues to show major disparities in diabetes outcomes across racial and socioeconomic groups. According to CDC and NIH analyses from recent years:

- Black Americans experience significantly higher diabetes complication rates than White Americans

- Hispanic communities also face elevated risks of diabetes-related hospitalization

- In some regions, diabetes mortality among Black populations remains 70–80% higher

These differences persist despite improvements in medication affordability. Why? Because insulin itself is only one part of diabetes care. Three major structural barriers continue to shape outcomes:

- Access to diabetes technology

- geographic access to pharmacies and care

- insurance design and hidden costs

Barrier 1: The Technology Gap

Modern diabetes management increasingly relies on medical technology. Two tools have become particularly important:

- Continuous Glucose Monitors (CGMs)

- Insulin pumps

These devices allow patients to track blood sugar levels in real time and adjust insulin dosing more accurately. They dramatically reduce the risk of severe complications. However, these technologies are not consistently covered by affordability policies. Research examining lower-income households shows significant disparities in access to these tools.

| Patient Demographic | CGM Access Rate (<$40k Income) | Pump Access Rate (<$40k Income) |

| White Youth | 27.9% | 25.5% |

| Black Youth | 15.2% | 12.9% |

This difference matters. Without continuous monitoring technology, patients often rely on less precise blood sugar tracking methods. That can lead to:

- higher complication risks

- more emergency hospitalizations

- long-term organ damage

The $35 insulin cap reduces medication costs, but technology affordability remains uneven.

Barrier 2: Pharmacy Deserts

Another often overlooked barrier is geographic access to pharmacies. Across both urban and rural America, many communities have seen pharmacy closures over the past decade. These areas are frequently referred to as pharmacy deserts. Residents in pharmacy deserts may face:

- long travel distances to the nearest pharmacy

- limited insulin brands in stock

- insurance network restrictions

- significant transportation costs

For patients without reliable transportation, accessing insulin may involve hours of travel or lost work time. Even with a $35 price cap, the real cost of obtaining medication can include:

- bus fares

- rideshare costs

- missed wages

- multiple pharmacy visits

These hidden costs rarely appear in national drug pricing debates, yet they shape daily healthcare decisions for many patients.

Barrier 3: The PBM “Middleman” Problem

Another unresolved issue lies behind the scenes of the pharmaceutical market: Pharmacy Benefit Managers (PBMs). PBMs act as intermediaries between:

- drug manufacturers

- insurance companies

- pharmacies

They negotiate rebates that determine which medications receive preferred placement on insurance formularies. Critics argue that this system encourages higher list prices. Here’s how the structure often works:

Typical PBM Pricing Flow

- Manufacturer sets a high list price

- PBM negotiates a rebate for formulary placement

- Insurance plans base coverage decisions on those negotiations

- Patients ultimately experience higher system costs through premiums or restricted drug choices

Even when patients themselves pay only $35, the broader system still operates around inflated list prices. In recent years, several state attorneys general have launched investigations into PBM practices, arguing that opaque rebate systems may contribute to rising healthcare costs. Transparency reforms remain under debate.

The Insurance Design Paradox

Even when insulin prices are capped, patients can still face significant financial strain due to insurance structure. Many marketplace plans rely on high deductibles to keep monthly premiums affordable. This creates a complicated financial dynamic.

Example Scenario

A patient finds a plan with capped insulin costs.

| Expense Type | Cost Structure |

| Insulin | $35 monthly cap |

| Specialist Visits | Full cost until deductible met |

| Lab Tests | Full cost until deductible met |

| CGM Sensors | Often partially covered or uncovered |

If the plan carries a $6,000 deductible, the patient may still pay thousands of dollars for other aspects of diabetes care. In effect, policy reforms have capped the price of the medication but not the overall cost of managing the disease.

The Growing Role of Technology in Insurance Decisions

Another emerging policy issue involves the increasing role of data analytics in insurance design. Many insurers now use predictive algorithms to:

- evaluate treatment adherence patterns

- analyze patient population risk profiles

- guide formulary placement decisions

These tools can potentially improve efficiency and reduce administrative costs. However, policymakers are also examining whether algorithmic decision-making could unintentionally reinforce existing disparities. If predictive systems rely on historical healthcare data, they may replicate patterns shaped by earlier inequalities in access to care.

As automated decision tools become more common in healthcare systems, regulators are increasingly discussing the need for transparency and oversight.

What a More Complete Solution Could Look Like

Moving beyond the insulin cap requires expanding policy attention to the broader ecosystem of diabetes care. Several reform priorities are frequently discussed by policymakers and healthcare researchers.

1. Expand Affordability to Diabetes Technology

Policies that cap insulin costs could be extended to essential diabetes management devices such as:

- Continuous glucose monitors

- insulin pumps

- sensor replacement supplies

These technologies play a direct role in preventing complications.

2. Increase Transparency in PBM Negotiations

Reforms targeting PBM rebate structures could:

- clarify how drug prices are set

- reduce incentives for high list prices

- improve competition among manufacturers

Greater transparency may also help regulators identify inefficiencies in the pharmaceutical supply chain.

3. Address Insurance Design for Chronic Conditions

Long-term illnesses like diabetes require consistent, ongoing care. Potential policy approaches include:

- reducing high deductibles for chronic disease management

- expanding preventive care coverage

- creating more predictable cost structures for long-term treatments

These reforms would shift policy focus from individual drugs to overall disease management.

The Next Phase of Insulin Policy

The $35 insulin cap marked a turning point in the national conversation around drug pricing. For millions of patients, the reform delivered immediate relief and reduced the fear of unaffordable medication. It demonstrated that large-scale policy interventions can meaningfully reshape pharmaceutical markets.

But the experience of the past few years also illustrates an important lesson in healthcare reform. Lowering the price of a single medication does not automatically resolve the larger system surrounding it. Diabetes outcomes remain shaped by access to technology, insurance design, geographic healthcare infrastructure, and the financial mechanisms that determine drug pricing behind the scenes.

The cap addressed one visible symptom of the crisis. The next phase of policy will determine whether the broader healthcare system can transform that progress into lasting, equitable access for everyone who depends on insulin.

")

{kind=link}